News website

other

How Forex Brokers Manage Risk: A-Book, B-Book, and Hybrid Models Explained

Brokeree Solutions

Brokeree Solutions

# How Forex Brokers Manage Risk: A-Book, B-Book, and Hybrid Models Explained

Advanced

Minimize operational risks

Mitigate dealing risks

## TL;DR

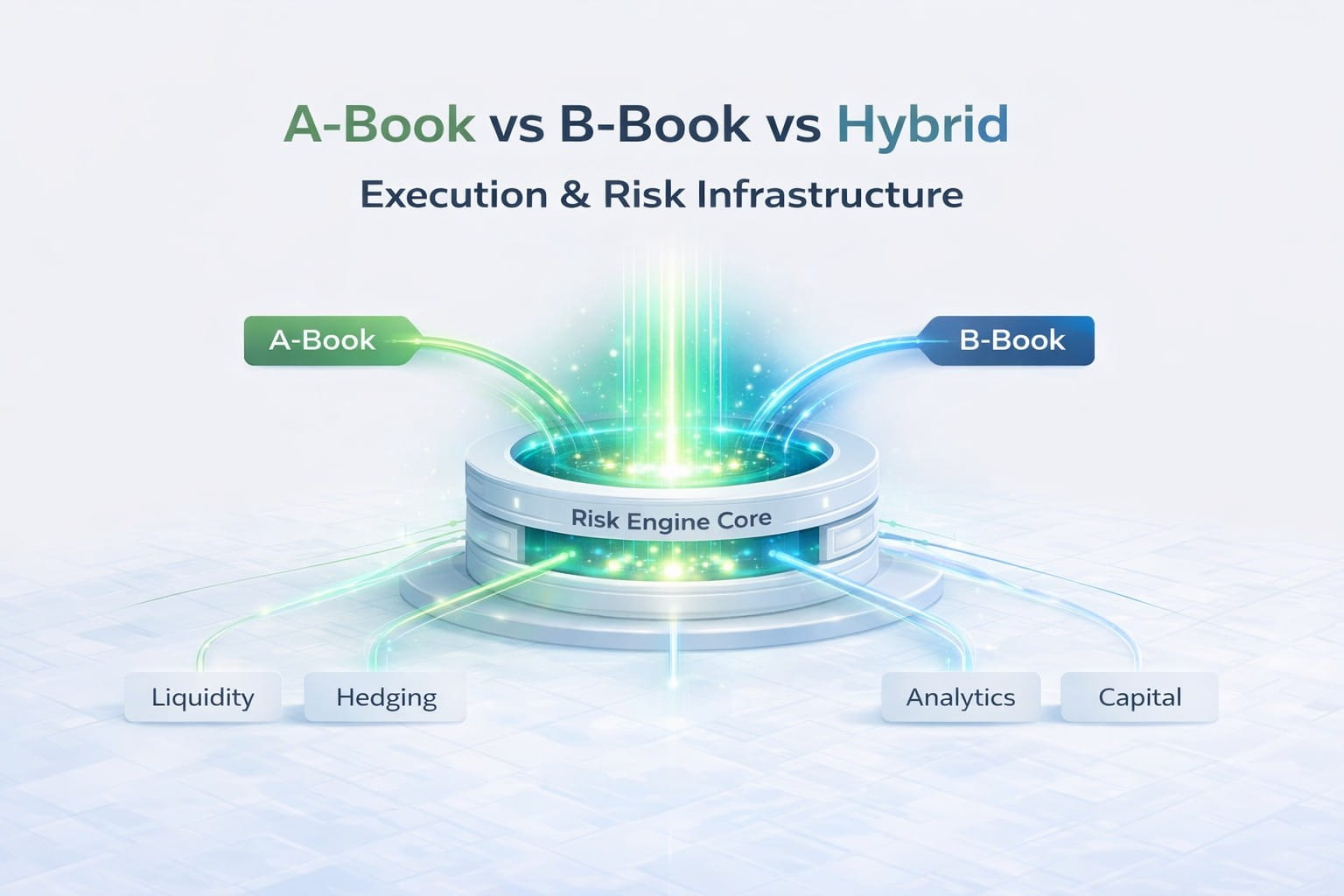

Forex brokers manage risk using three primary execution models:

- A-Book (Agency Model): Client trades are passed to liquidity providers. Brokers earn commissions or spread markups and carry minimal market risk.

- B-Book (Market Maker Model): Brokers internalize client trades and take the opposite side of positions. Here, brokers generate revenue through spreads and net internalized flow. They manage risk through hedging and structured risk controls.

- Hybrid Model: A strategic mix of both, routing some trades externally while internalizing others based on risk profiles.

The right model depends on capital, client profile, trading volume, regulation, and technology infrastructure. Modern brokers rely on bridges, dealing desks, and real-time analytics to balance profitability with client protection.

## **How Forex Brokers Manage Risk: A-Book, B-Book, and Hybrid Models Explained**

Retail forex brokerage is about risk control. Every time a trader opens a position, the broker must ask themselves the following questions:

- Should this trade be passed to the market?

- Should it be kept internally?

- Or should it be partially hedged?

Whatever the answer is determines the broker’s risk exposure.

For example, imagine a broker with 10,000 retail clients trading EUR/USD during a volatile session. If most clients are buying and the market suddenly drops 200 pips, someone absorbs that loss. Depending on the execution model, it may be liquidity providers or the broker.

In the retail and institutional forex brokerage environment, choosing the right execution model directly impacts a broker’s profitability, regulatory positioning, and long-term stability. Whether operating as a market maker (B-Book broker), a Straight Through Processing (STP) broker, or a hybrid structure, the decision shapes how risk is transferred, internalized, or hedged.

This is why the execution model you choose as a broker defines your capital requirements, revenue stability, technology needs, regulatory exposure, and reputation risk. Understanding A-Book, B-Book, and Hybrid models is your first step to expertly managing that exposure.

**DID YOU MISS:** **[A-Book vs B-Book: What’s the Difference?](https://brokeree.com/articles/a-book-vs-b-book-whats-the-difference/)**

## **A Note on the A-Book vs B-Book Debate**

The A-Book vs. B-Book discussion is often oversimplified. In reality, the distinction is not about “good vs bad” or “safe vs risky.”

A key clarification raised in industry discussions is the difference between:

- Regulatory capital requirements

- Liquidity-side working capital (margin/prefunding with LPs)

When discussing “capital requirements,” it is important to separate statutory regulatory capital from the operational capital required to execute and hedge trades.

For example, a pure A-Book broker may carry minimal directional exposure. But typically must post margin or prefund accounts with liquidity providers and prime brokers. That ties up working capital.

A pure B-Book broker does not need to prefund LPs for every trade. But must maintain sufficient capital buffers to absorb aggregate client P&L swings and tail-risk events.

In other words, someone always holds the risk. The real question is how that risk is managed, capitalized, and disclosed.

This article focuses on execution mechanics and operational capital. Not legal capital thresholds, which vary by jurisdiction.

## **A-Book vs B-Book vs Hybrid: Definitions Explained**

### A-Book Model (Agency / STP Risk Transfer)

In the A-Book model, brokers transfer client trades directly to **[liquidity providers](https://brokeree.com/solutions/liquidity-providers/)** (LPs). This can be banks or non-bank market makers. When a client buys 1 lot of EUR/USD, the broker simultaneously enters an identical trade with a liquidity provider. That way, the broker earns commission per lot traded and spreads markup.

Because client trades go to external liquidity providers, the broker minimizes direct directional risk. However, A-Book execution still involves operational, counterparty, margin, and execution risks. These risks often come during periods of extreme volatility or reduced market liquidity.

This model is commonly associated with Straight-Through Processing (STP) brokers and Electronic Communication Network (ECN) brokers.

Strengths:

- Reduced direct directional market exposure;

- Access to institutional liquidity;

- Transparent pricing.

While A-Book brokers reduce directional exposure, they are still exposed to:

- Counterparty risk (LP default or execution failure);

- Slippage and liquidity gaps;

- Margin calls from prime brokers;

- Negative balance events in extreme volatility.

The **[2015 Swiss National Bank](https://trademakers.com/2023/06/15/cautionary-tales-of-poor-risk-management-4-the-2015-swiss-franc-shock/)** (SNB) event is a widely cited example. When the EUR/CHF floor was removed, liquidity evaporated. A-Book brokers like FXCM suffered as liquidity providers stopped providing pricing during [**the event**](https://www.globenewswire.com/news-release/2015/03/12/714464/33730/en/FXCM-Releases-Detailed-Data-on-the-SNB-Flash-Crash.html). This resulted in some clients having negative balances, as there was no way to execute stops in time. The broker ended up on the hook for those negative balances. A-Book reduces client-risk conflict, but it does not eliminate operational or counterparty risk.

### B-Book Model (Market Maker/Internalization)

In the B-Book model, the broker takes the opposite side of client trades. If a client buys EUR/USD, the broker actually sells it to them internally. Trades remain “in the broker’s book.”

Brokers get revenue from spread income and net internalized flow. While retail trading outcomes vary **[statistically](https://acy.com/en/market-news/education/reasons-retail-traders-fail-profitable-trading-j-o-194343/)** across client segments, brokers actively manage their risk through hedging strategies, position netting, and predefined risk limits to maintain capital stability.

Unlike STP or ECN models, a dealing desk broker internalizes order flow and manages exposure internally, often referred to as the market-maker model.

Strengths:

- Faster internal execution

- Stable spreads

- Potentially higher margins

Risks:

- Direct market exposure

- Conflict-of-interest perception

- Regulatory scrutiny

Consider a broker with $50M in client exposure during a strong bullish move. If most clients are long and profitable, the broker must pay those profits. Without proper hedging or segmentation, this can quickly affect capital reserves.

B-Book profitability relies heavily on disciplined risk management. This skill involves risk monitoring and the broker’s ability to hedge strategically when aggregate risk exceeds predefined limits.

### Hybrid Model (Selective Routing / C-Book)

The Hybrid model combines A-Book and B-Book strategies. Here, brokers analyze client behavior and segment traders.

Hybrid execution is not a fixed three-bucket system. It is a dynamic risk allocation framework. Modern brokers do not segment clients once and leave them there. Instead, routing decisions are continuously adjusted based on:

- Real-time net exposure per instrument;

- Client profitability over rolling periods;

- Order size relative to available liquidity;

- Volatility regime (calm vs stressed markets);

- Correlation risk across instruments;

- Margin utilization and capital thresholds.

For example, a trader may be internalized during low volatility but automatically hedged during high-impact news events. Likewise, exposure may be partially offset when instrument-level concentration exceeds predefined risk limits.

Hybrid execution, therefore, is not about labeling t

This brief was generated from the original reporting. Read the full article at the source:

Read at brokeree.com