Regulation and incorporation

regulatory

ASIC lifts bonnet on car finance costs and distribution concerns

ASIC

ASIC

[Newsroom](https://www.asic.gov.au/newsroom)

PrintShare

- [X Opens in new window](https://twitter.com/intent/tweet?url=https%3A%2F%2Fwww.asic.gov.au%2Fabout-asic%2Fnews-centre%2Ffind-a-media-release%2F2026-releases%2F26-132mr-asic-lifts-bonnet-on-car-finance-costs-and-distribution-concerns%2F&text=ASIC%20lifts%20bonnet%20on%20car%20finance%20costs%20and%20distribution%20concerns)

- [Facebook Opens in new window](https://www.facebook.com/sharer.php?u=https%3A%2F%2Fwww.asic.gov.au%2Fabout-asic%2Fnews-centre%2Ffind-a-media-release%2F2026-releases%2F26-132mr-asic-lifts-bonnet-on-car-finance-costs-and-distribution-concerns%2F)

- [LinkedIn Opens in new window](https://www.linkedin.com/shareArticle?mini=true&url=https%3A%2F%2Fwww.asic.gov.au%2Fabout-asic%2Fnews-centre%2Ffind-a-media-release%2F2026-releases%2F26-132mr-asic-lifts-bonnet-on-car-finance-costs-and-distribution-concerns%2F)

- [Email Opens in new window](mailto:?subject=ASIC%20lifts%20bonnet%20on%20car%20finance%20costs%20and%20distribution%20concerns&body=An%20article%20from%20ASIC%3A%0D%0A%0D%0AASIC%20lifts%20bonnet%20on%20car%20finance%20costs%20and%20distribution%20concerns%0D%0A%0D%0Ahttps%3A%2F%2Fwww.asic.gov.au%2Fabout-asic%2Fnews-centre%2Ffind-a-media-release%2F2026-releases%2F26-132mr-asic-lifts-bonnet-on-car-finance-costs-and-distribution-concerns%2F)

ASIC has put car finance providers on notice after identifying a range of concerns in relation to third party distributor arrangements, sales practices and monitoring of consumer outcomes.

ASIC’s review examined data from over 350,000 loans across eight car finance providers, including some of Australia’s largest. It identified shortcomings in some lenders’ oversight of distributors like brokers and car dealers who sell their loans, exposing consumers to harm.

ASIC Commissioner Alan Kirkland said the findings, released today in Report 832 _Lifting the bonnet: ASIC's review of car loans_( [REP 832](https://www.asic.gov.au/regulatory-resources/find-a-document/reports/rep-832-lifting-the-bonnet-asic-s-review-of-car-loans/ "REP 832 Lifting the bonnet: ASIC's review of car loans")), indicate that some lenders are not paying enough attention to the impact of their practices on consumers.

‘Lenders should be monitoring the experiences of borrowers, especially where loans are sold by third parties like dealers or brokers. Responsibility for consumer outcomes cannot be outsourced.

‘This review lays bare the potential risks when lenders fail to effectively monitor third-party distributors, and how consumers can pay the price.’

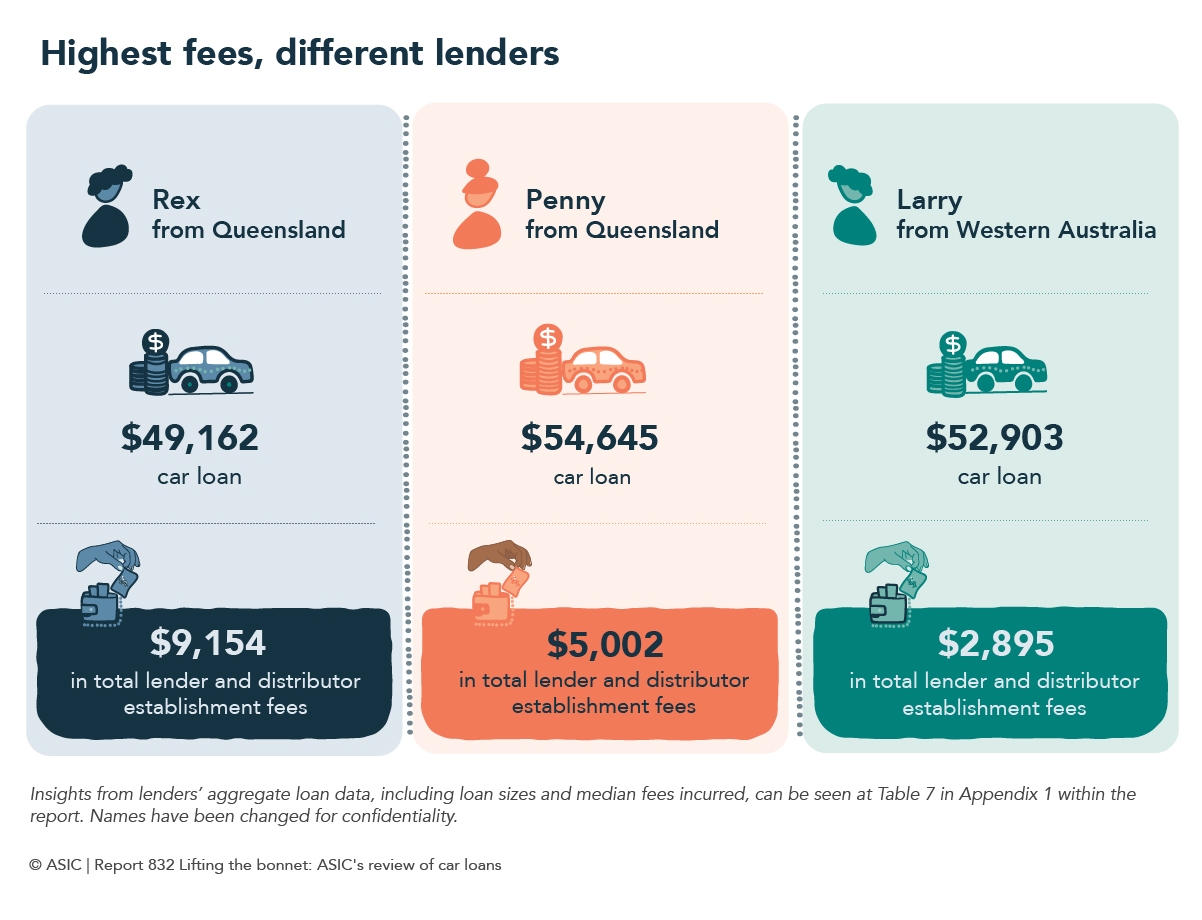

ASIC found that the overall cost of car loans could vary widely and that total fees could be significant, particularly for relatively low-value loans.

Loans typically incurred two establishment fees—a lender establishment fee, ranging from $299 to $995, and a distributor establishment fee, ranging from a flat fee of $912 to up to $2,500.

However, one lender—charging the highest total fees across all loans reviewed—also imposed a third fee, with one customer paying over $9,000 in fees on a $49,162 car loan. This included over $7,800 to the lender and $1,320 to the broker—around 18% of the total loan amount.

### Infographic – Highest fees, different lenders (text version)

Column 1

- Rex from Queensland

- $49,162 car loan

- $9,154 in total lender and distributor establishment fees

Column 2

- Penny from Queensland

- $54,645 car loan

- $5,002 in total lender and distributor establishment fees

Column 3

- Larry from Western Australia

- $52,903 car loan

- $2,895 in total lender and distributor establishment fees

Insights from lenders’ aggregate loan data, including loan sizes and median fees incurred, can be seen at Table 7 in Appendix 1 within the report. Names have been changed for confidentiality.

© ASIC \| Report 832 Lifting the bonnet: ASIC's review of car loans

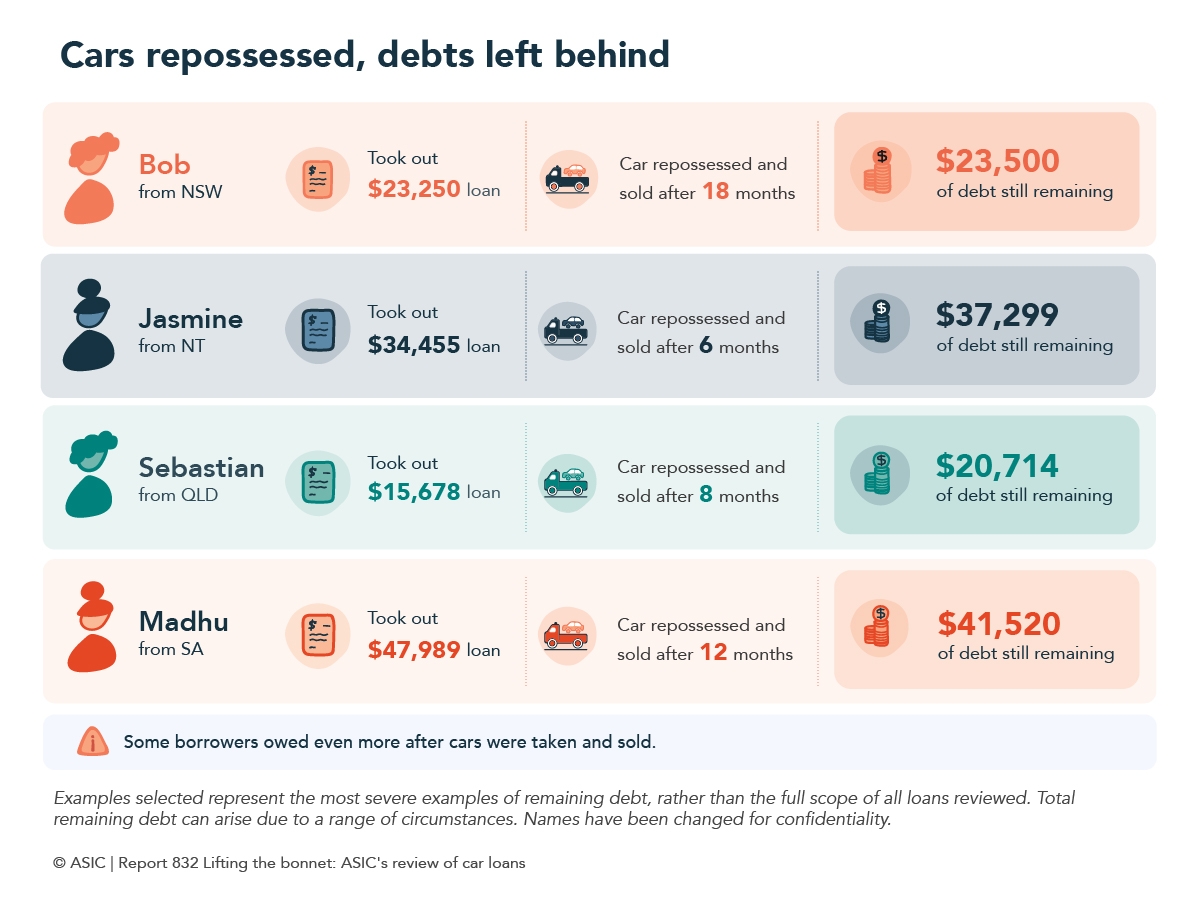

ASIC also found that when consumers fell into hardship, some received inconsistent hardship support, while for those whose cars were re-possessed and sold, many still owed their lender money.

‘Consumers shouldn’t lose their car and still be stuck with the bulk of their debt,’ Mr Kirkland said.

However, in a sample of 250 loans reviewed, 90% of consumers still owed over half their total loan amount, and in some cases over 100% of the loan amount.

### Infographic – Cars repossessed, debts left behind (text version)

Row 1: Bob

- Bob from NSW

- Took out $23,250 loan

- Car repossessed and sold after 18 months

- $23,500 of debt still remaining

Row 2: Jasmine

- Jasmine from NT

- Took out $34,455 loan

- Car repossessed and sold after 6 months

- $37,299 of debt still remaining

Row 3: Sebastian

- Sebastian from QLD

- Took out $15,678 loan

- Car repossessed and sold after 8 months

- $20,714 of debt still remaining

Row 4: Madhu

- Madhu from SA

- Took out $47,989 loan

- Car repossessed and sold after 12 months

- $41,520 of debt still remaining

Some borrowers owed even more after cars were taken and sold.

Examples selected represent the most severe examples of remaining debt, rather than the full scope of all loans reviewed. Total remaining debt can arise due to a range of circumstances. Names have been changed for confidentiality.

© ASIC \| Report 832 Lifting the bonnet: ASIC's review of car loans

‘If a large proportion of customers are falling behind on repayments early, it raises serious questions about whether those loans were appropriate in the first place and how lenders conduct their affordability checks,’ Mr Kirkland said.

He also pointed to the importance of how lenders verify the value of vehicles, including in situations where over-valuation creates higher risks for consumers, such as for older cars with high mileage in remote areas.

Through its review, ASIC found that a consumer’s location and chosen lender could affect their outcomes, particularly in regional and remote locations, with participating lenders approving a lower proportion of hardship variations in these locations than others.

ASIC’s intervention has already driven some changes across the car finance sector, with all eight participating lenders improving hardship processes, and many strengthening product distribution conditions, product review triggers, governance and oversight of high-volume distributors to better detect and respond to consumer harm.

Commissioner Kirkland said that while it was encouraging to see some improvements to lenders’ processes, much more needed to be done to improve practices across the sector.

‘Australians shouldn’t be at risk of financial harm simply because they need a car to get to school, work and essential services,’ Mr Kirkland said.

‘Lenders and intermediaries need to put consumers at the centre of how these products are designed, sold and serviced, and fix practices that leave too many drivers worse off.

‘We will be monitoring the progress of lenders involved in this work, and where we identify lenders or intermediaries failing to comply with legislative obligations, will take action to address consumer harm.’

## Background

ASIC’s review looked at the experiences of consumers in the motor vehicle finance sector.

ASIC’s probe considered the compliance of participating lenders, including their oversight of distributors, such as brokers and dealerships, and reviewed how loan defaults, hardship practices and dispute resolution processes are managed.

Lenders involved in the review:

- Australian Alliance Automotive Finance Pty Ltd

- Angle Auto Finance Pty Ltd

- Latitude Automotive Financial Services

- Nissan Financial Services Australi

This brief was generated from the original reporting. Read the full article at the source:

Read at asic.gov.au