Broker

other

Pricing Models in Event-Based Trading: How Brokers Generate Revenue

Leverate LXCRM

Leverate LXCRM

# Pricing Models in Event-Based Trading: How Brokers Generate Revenue

- June 16, 2026

# **Pricing Models in Event-Based Trading: How Brokers Generate Revenue**

The mechanics of how a broker makes money from a prediction market are not as straightforward as they first appear. Event-based trading sits at an intersection of financial product design and content management, and the pricing model a broker chooses shapes not just margin per trade, but the behaviour of the entire trader base. Charge too much and traders migrate to platforms with lower friction. Charge too little and the product runs at a loss that only heavy volume can offset.

Brokers evaluating pricing models in event-based trading often underestimate how much pricing architecture influences participation patterns. This article examines the main models in use, how they perform in practice, and the operational decisions brokers need to make before committing to a structure.

## **What Pricing Models Mean in Prediction Markets**

In conventional financial products such as CFDs or forex, the pricing model is well established: spreads, commissions, or a combination of both. In event-based trading, the equivalent concept is how the broker captures a margin on each binary outcome market without making the cost so visible that it deters trading activity.

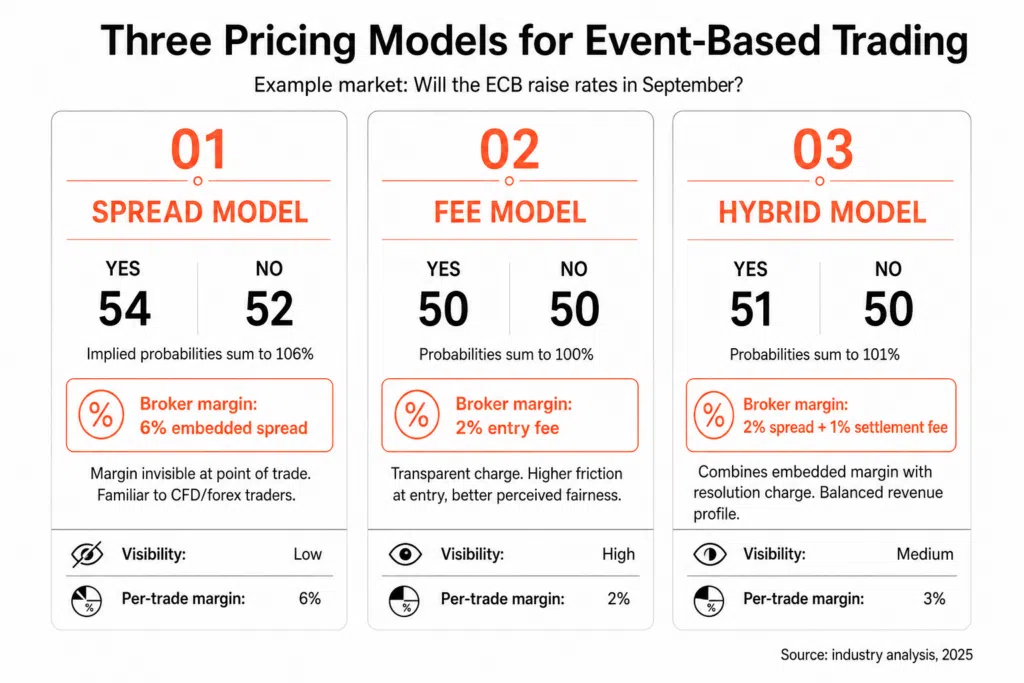

Pricing models in event-based trading typically fall into two broad categories. The first is a spread-based model, where the sum of the probabilities offered on both sides of a binary outcome exceeds 100%, with the gap representing the broker’s margin. The second is a fee-based model, where traders pay a flat or percentage charge to enter or exit a position, and the market probabilities sum closer to 100%.

A third approach, used by some operators, is a hybrid that applies a small embedded spread alongside a withdrawal or settlement fee. Each model has different implications for how traders perceive value, how frequently they trade, and how much the broker earns per resolved event. The choice is not simply a pricing decision; it is a product design decision with consequences for retention, volume, and long-term commercial viability.

The spread model offers a natural familiarity advantage for operators and traders accustomed to CFD or forex products. The broker’s margin is built into the price rather than applied as a separate charge, which reduces the psychological friction at the point of entry. A trader who sees a Yes position priced at 52 and a No position priced at 52 knows that the two sides do not sum to par, but the experience of entering the trade is not interrupted by a fee deduction.

The practical challenge with the spread model in event-based trading is that thinner markets, those with lower volume or fewer participants, can require wider spreads to manage the broker’s exposure. Wider spreads in turn make the pricing less competitive and can further reduce participation. This dynamic requires careful calibration per market category, and operators who set spreads uniformly across all categories tend to find that some markets are chronically under-traded as a result.

According to a 2025 analysis by Finance Magnates examining the growth of binary and event-based trading products, platforms that offered transparent fee structures alongside competitive spreads reported better trader retention than those relying on opaque embedded margins alone.

**Source:** [Finance Magnates, 2025](https://www.financemagnates.com/)

Fee-based models offer greater transparency but require the broker to justify the charge at the point of trade entry. Flat fees work well for higher-value markets where the fee represents a small percentage of the position. Percentage fees scale naturally with position size but can become prohibitive for small-stake traders, which affects the accessible market and the demographic mix on the platform.

## **How Brokers Generate Revenue from Prediction Markets**

Beyond the per-trade margin, brokers operating prediction markets have several secondary revenue streams to consider. Settlement fees charged at the point of resolution are one option. Some operators charge for premium market access, giving certain account tiers earlier access to new markets or tighter pricing on popular events. Others incorporate prediction market activity into a broader loyalty or deposit bonus structure, using the product as a retention tool rather than a standalone revenue line.

The revenue profile of pricing models in event-based trading also depends on the resolution cycle. A market that resolves in 24 hours generates a faster revenue cycle than one that resolves over 30 days, but the short-cycle market may carry higher content management overhead to keep the event pipeline filled. Brokers need to model both the per-trade margin and the cost of maintaining the content operation before drawing conclusions about product profitability.

| | | | |

| --- | --- | --- | --- |

| **Revenue Source** | **Model Type** | **Volume Dependency** | **Predictability** |

| Embedded spread | Spread-based | High | Medium |

| Entry/exit fee | Fee-based | High | High |

| Settlement fee | Hybrid | Medium | Medium-High |

| Premium tier access | Subscription | Low | Very High |

## **How Pricing Impacts Trading Volume**

The relationship between pricing models in event-based trading and volume is not linear. Research into behavioural patterns in binary outcome markets suggests that trader sensitivity to pricing depends heavily on how the cost is presented. An embedded spread of 6% on a binary market may produce less resistance than a visible 3% entry fee, even though the former is twice the cost, because the latter requires the trader to consciously register the charge at the moment of decision.

This has practical implications for how brokers configure their pricing. Markets with strong public awareness, such as major election outcomes or scheduled central bank decisions, can typically sustain higher spreads because trader motivation is driven by interest in the event rather than price optimization. Niche markets with smaller potential audiences are more price-sensitive and may require tighter spreads or reduced fees to reach meaningful volume.

Volume also affects the broker’s ability to manage the risk side of event-based trading. A market with thin participation on one side creates an imbalanced book, which may require the operator to take on residual exposure or to adjust pricing to attract the underrepresented side. Automated pricing adjustment tools, which can widen or narrow spreads based on book balance, are becoming a standard component of well-designed event-based trading infrastructure.

## **Balancing Profitability and User Growth**

The tension between margin capture and user growth is a consistent feature of pricing model decisions in event-based trading. A pricing structure optimised purely for margin per trade may perform well in the short term but creates the conditions for trader churn as users become aware of more competitively priced alternatives. A structure optimised for growth, with very thin margins, can drive volume but may not be commercially sustainable unless scale is achieved quickly.

Operators with the most sustainable revenue models tend to use pricing model differentiation

This brief was generated from the original reporting. Read the full article at the source:

Read at leverate.com